What is a Mpesa statement?

A Mpesa Statement is a report that shows the transactions you have made via Mpesa for a certain period of time.

There are two types of statements; a mini statement and a full statement.

How to get Mpesa mini statement

It only shows your recent Mpesa transactions that are more than an hour old and can only show a maximum of 5 transactions.

A mini statement is received in form of a text message ( SMS).

To obtain your Mpesa mini Statement use the steps below;

Dial *234#

Go to ‘My Mpesa Information’

Key in the number 2 and press send.

Choose ‘Mpesa statement’

Key in the number 1 and press send.

Select ‘Mini Statement’

How to get full Mpesa statement

Dial *234# and Select ‘My Mpesa Information’

Key in the number 2 and press send.

Select ‘Mpesa statement’

Key in the number 1 and press send.

Select ‘Full Statement’

Key in your ID or passport number.

Input your email address.

Ensure that your email address is correct.

Select the period which you would like to receive the statement.

You will receive a text message of successful registration.

Your Mpesa statement will be sent to the email address in less than 5 minutes.

How to download Mpesa statement online

Access your email account and scroll to the Safaricom email containing your statement.

The email containing the Mpesa statement is password protected.

When prompted for a password all you have to do is key in your identification document registered with your Mpesa line.

That could be either of the following;

National ID

Passport

Military ID

Diplomatic ID

Alien ID

How to Check your M-PESA Statements Online

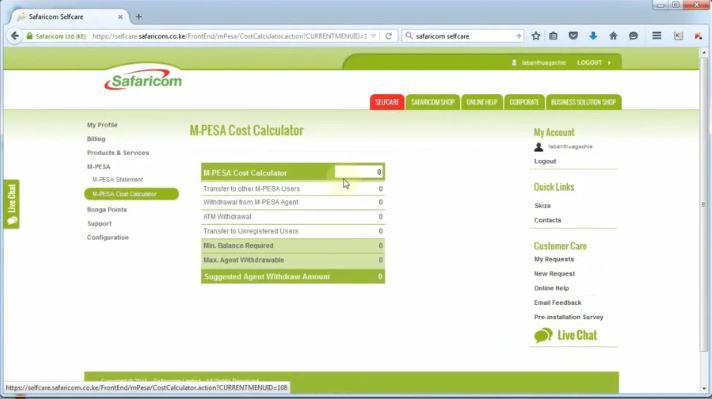

It is possible to download your Mpesa statement online by accessing Safaricom Self-care.

Safaricom’s self-care allows users the ability to manage their Safaricom account online

Simply type in the URL www.safaricom.co.ke.

Click on self-care

Choose the kind of registration you would like to do,

Select individual if it is for your personal use

Type in your mobile number and username

Agree to the terms and condition and an activation number will be sent to your phone.

Key in the activation number and the process is complete.

Safaricom portal login requests for the same username and password you filled in during registration so be sure not to forget it.

After completing the necessary details you should get a verification SMS on your phone.

Note: You can even choose a specific timeline (e.g 3 months, 2 weeks) since you’re provided with a calendar to choose specific dates.

The timeline, however, is only valid for a period of 6 months.

If you need M-PESA statements for more than 6 months, use the USSD option to get one for 12 months. For anything beyond that, Safaricom advises you to visit a Safaricom shop and make the request there.

How to get Mpesa statement using Safaricom M-ledger

You can also get your Mpesa statement using the M-ledger Mpesa app that scans your existing Mpesa text messages on your phone and afterward creates a database from them.

The higher the amount of Mpesa information one has on the phone, the more information M-Ledger will have to process.

Download M-ledger from your android Appstore to get your Mpesa transaction statements.

The app also does the following:

It imports up to 6 months of your M-PESA transactions into the app

Shows your current M-PESA balance

Shows your recent transactions

Has an M-PESA calculator to calculate transaction costs

Shows the total amount sent and received over a period time

Shows transactions per person or business

Shows you your top 20 M-PESA money recipients and senders

Sorts total amounts transaction type i.e. airtime, paybill, buy goods, deposit, withdrawal, sent

Automatically backups and restores your transactions from the cloud

Summarizes most of this data in graphs and charts

Benefits of M-ledger

It’s convenient, easy to use and does a good job analysing your transactions into nice readable formats, unlike the statements which just report the data as it is.

It’s also the only method here that give you direct access to M-PESA statements beyond 6 months one year assuming you have the M-PESA transaction SMS messages in your phone.

You can also visit the M-Ledger website and from there you can generate spreadsheets (Excel) of your transactions and also export the data to PDF, Word etc.

This must come in handy for business owners that use M-PESA.

What to do when M-PESA statement has a disclaimer

If the statement has a disclaimer indicating that it cannot be used in court, then you should do the following:

You need to visit the nearest Safaricom retail shop and inform them that you would like an M-PESA statement for court purposes.

You will be provided with a form for which you will indicate your details and also provide your national ID.

A request will be created for processing.

You may collect your statement after a minimum of 5 business days.

What to do when a relative passes on and you need to obtain their Mpesa funds

Visit your nearest Safaricom retail shop with the following documents:

Your ID

A copy of the deceased’s death certificate (burial permits are not allowed)

An affidavit indicating your relationship with the deceased

A letter from the local county administration/chief in the deceased’s area of residence

Note:

1. For M-PESA accounts containing amounts more than Ksh 30,000 you will need to provide the following documents:

Your ID

A copy of the deceased’s death certificate (burial permits are not allowed)

A Grant of Probate/ Grant of Letters of Administration intestate/ a letter from the public trustee

2. For M-PESA accounts containing amounts less than KES 30,000 you will need to provide the following documents:

Your ID

A copy of the deceased’s death certificate (burial permits are not allowed)

Letter from the county administration/ chief in the deceased’s area of residence

Once the above documents are provided, you will be required to fill in a claim form and nominate an M-PESA registered number to which we can transfer the funds within 72 hours.